Post-pandemic shifts have broken the traditional real-estate cycle. Demand is no longer rebounding evenly, but concentrating in top-tier spaces, leaving weaker offices behind and forcing cities to rethink how to repurpose surplus supply.

Commercial real estate has traditionally followed a predictable pattern. Demand rises while supply lags, prompting construction that eventually creates oversupply and falling prices. However, the office space sector seems to be breaking this cycle. After Covid-19 fuelled a push towards remote work, the demand for office space has been structurally lower rather than cyclical, and the typical excess supply period has not been followed by the typical recovery period.

The result of this structural change is what appears to be a longstanding mismatch between supply and demand. Real estate is not a liquid asset, and office buildings are long-duration assets financed with debts that have long amortization periods. The supply of office space seemingly cannot be reduced enough to meet the newly diminished demand. However, office space might not be as doomed as many predict for 3 key reasons.

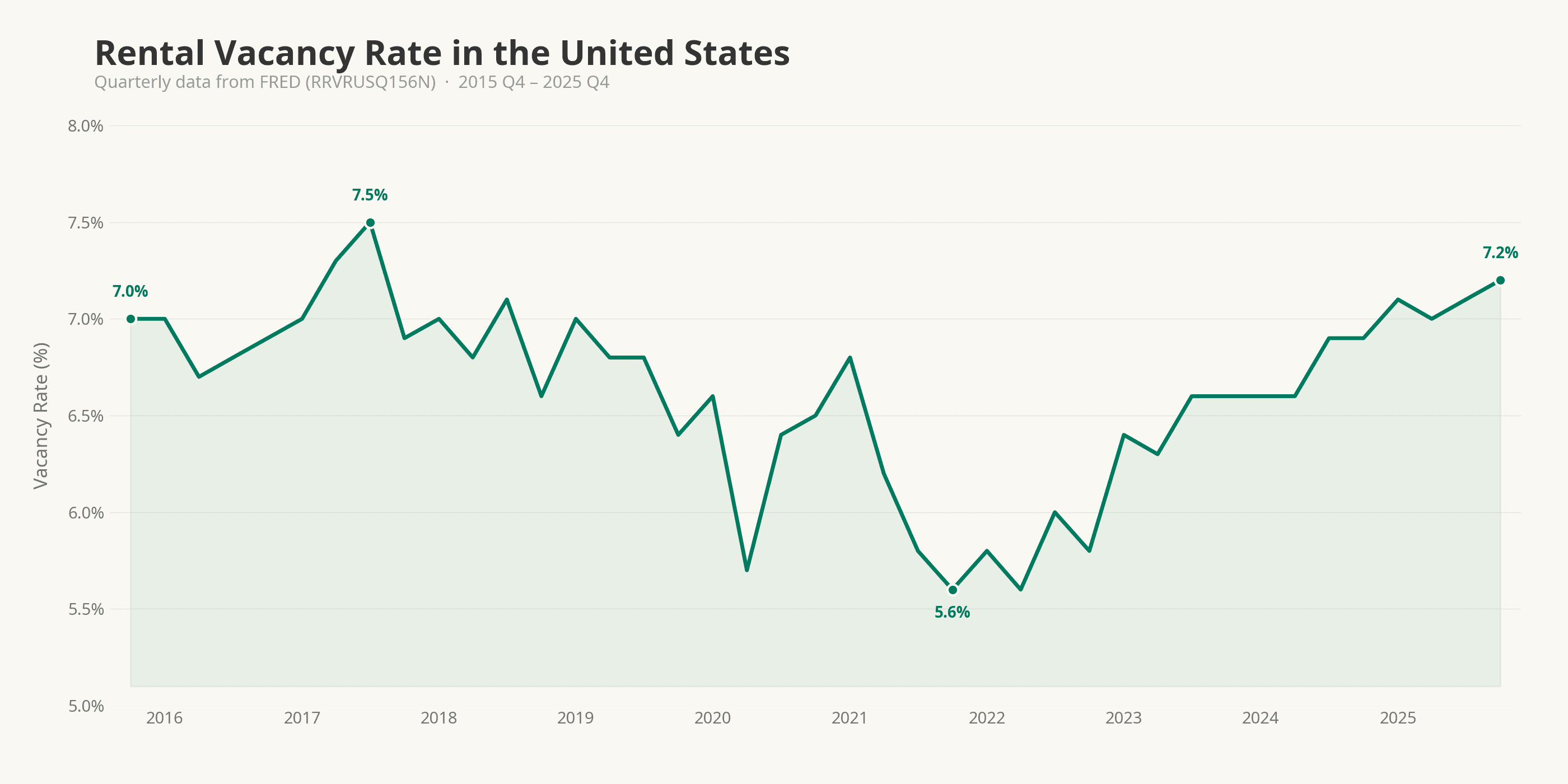

The trend in vacancy rates further illustrates the distinction between cyclical and structural shifts. As shown in the data, vacancy rates fell sharply during the pandemic before gradually rising again, suggesting a typical cyclical recovery pattern rather than a permanent collapse in demand. However, this recovery masks bigger changes in how space is used. Unlike previous cycles, where falling vacancy signaled renewed demand across the market, the current environment reflects uneven demand concentrated in higher-quality properties, while weaker assets continue to struggle. In this sense, the apparent normalization in vacancy rates does not contradict the argument of structural change, but rather highlights how aggregate data can obscure a growing divergence within the office market.

First, a push towards office-to-residential conversions may slightly ease supply. This approach has had mixed success so far; comparing New York City, Miami, and San Francisco reveals three very different pictures. New York has had the most success, with 4.1 million square feet of conversions started in 2025 and 8,300 apartments in the pipeline. Miami has seen limited success, with 212 apartments planned. San Francisco has not had a single conversion. New York has seen so much success because of aggressive tax incentives, streamlined local government, a large stock of pre-1960s office buildings, and high demand for residential space. San Francisco, in contrast, has more zoning and regulatory constraints, a much newer office stock, and a relatively weaker demand for residential space.

Second, some demand is increasing. The flight-to-quality phenomenon, most visible in New York City, has generated significant demand for Class A office space. Vacancy rates have rebounded to just 14%, and major employers, including financial firms and law firms, are signing long-term leases for premium, amenity-rich spaces. Although Class B and C buildings are failing, Class A buildings are nearly full. This suggests that the office market is not dying, but rather bifurcating, with the strongest assets pulling ahead and the weakest becoming effectively obsolete.

Third, and most importantly, although supply is inelastic and demand has shifted structurally, policy interventions are beginning to affect incentives. New York has rolled out massive incentives, including a $467 million tax credit for conversions, and Mayor Mamdani has pushed to accelerate permitting and zoning approvals to help the market self-correct faster. Other cities are beginning to follow suit, recognizing that prolonged vacancy is a fiscal and civic liability, both in regard to wasted tax dollars and area safety.

Given the above, the most likely outcome would be that cities that combine aggressive policy, older building stock, and robust residential demand, such as New York, Washington D.C., and Chicago. will find a path through the uncertain office market, while other cities will face much longer and more painful stock shedding. The office is not dead, but it is being permanently reorganized around the question of what makes the buildings worthwhile.