Macroeconomics Chapter 19: Financial Sector

This chapter explores the concept of the financial sector, which has been seen as a most important part of the macroeconomy.

The Financial Sector

The financial sector occupies a central position in the functioning of a modern economy. It provides the institutional framework through which saving is transformed into investment, enabling resources to be allocated across time and between different economic agents. The importance of the financial sector has become especially apparent since the global financial crisis of the late 2000s, which highlighted both the essential role that financial institutions play in supporting economic activity and the serious consequences that arise when financial systems malfunction.

In developing and emerging economies, the financial sector is often viewed as a critical constraint on economic growth and development. The ability to raise finance for investment projects, to fund infrastructure, and to support the expansion of productive capacity depends heavily on the existence of effective financial institutions and markets. Where these institutions are absent or underdeveloped, economic activity may be limited even when profitable investment opportunities exist. This chapter examines the role of the financial sector in facilitating saving and investment, its contribution to economic growth and development, and the ways in which access to finance can be expanded.

The role of the financial sector

The financial sector provides the environment in which economic activity takes place by performing several interconnected functions. At its core, it acts as an intermediary between those economic agents who wish to save and those who wish to borrow. By bringing together savers and borrowers, the financial sector enables resources that are not currently being consumed to be used to finance investment and future production.

One key role of the financial sector is the facilitation of saving. Households and firms may wish to save for a variety of reasons, including future consumption, retirement, precautionary motives, or the accumulation of funds for large purchases such as housing or capital equipment. Financial institutions provide mechanisms through which saving can take place in a secure and organized manner. By offering deposit accounts and other financial assets, the financial sector allows savers to earn a return on funds that would otherwise remain idle. However, when interest rates are very low, the incentive to save through formal financial channels may be weakened.

Closely linked to saving is the facilitation of borrowing. Firms and households often require access to funds in order to undertake expenditure that exceeds their current income. Firms may wish to borrow in order to finance investment in physical capital, research, or expansion, while households may borrow to smooth consumption over time or to purchase durable goods such as homes. Financial markets and institutions provide opportunities for borrowers to obtain loans, while interest rates act as the price that balances the supply of savings with the demand for borrowing.

Beyond facilitating saving and borrowing, the financial sector plays a crucial role in enabling the exchange of goods and services. A stable and reliable financial system supports transactions by providing payment mechanisms that reduce transaction costs and increase efficiency. In situations where inflation is very high, economic agents may attempt to minimize their holdings of money by making frequent trips to financial institutions or rapidly converting money into goods. Such behavior increases transaction costs and undermines the smooth functioning of markets, highlighting the importance of financial stability.

The financial sector also supports economic activity through the provision of forward and futures markets. These markets allow economic agents to enter into contracts for future delivery at agreed prices, reducing uncertainty and risk. This is particularly important in markets characterized by volatile prices, such as commodities and foreign exchange. By allowing firms to hedge against price fluctuations, financial markets help stabilize investment and production decisions.

Another major component of the financial sector is the market for equities. Equity markets allow firms to raise finance by selling ownership stakes to investors, providing an alternative to borrowing. For investors, equity markets offer the possibility of sharing in future profits. The existence of well-functioning equity markets therefore supports long-term investment and economic growth.

The financial sector in developing and emerging economies

In developing and emerging economies, the financial sector often faces significant challenges that limit its effectiveness. Formal financial institutions may be poorly developed, and access to banking services may be limited, particularly in rural areas. Stock markets may be absent or operate inefficiently, reducing opportunities for firms to raise finance through equity issuance.

One important issue in these economies is asymmetric information. Borrowers typically possess more information about the risks and potential returns of investment projects than lenders do. As a result, banks may find it difficult to assess creditworthiness accurately, leading to higher interest rates or credit rationing. Weak property rights and insecure land ownership can further exacerbate this problem by making it difficult for borrowers to provide collateral.

When access to formal financial institutions is limited, households and firms may turn to informal credit markets. These markets often involve local moneylenders who possess monopoly power and charge very high interest rates. While informal credit may provide short-term access to funds, it can also trap borrowers in cycles of debt and limit long-term development.

Despite these challenges, the financial sector remains a crucial component of the development process. Effective financial institutions can mobilize savings, allocate capital to productive uses, and support investment in both physical and human capital. The extent to which the financial sector succeeds in performing these roles has significant implications for economic growth and living standards.

Saving and investment

For developing and emerging economies, a central objective is to achieve sustained economic growth that raises living standards and supports human development. From a macroeconomic perspective, growth can be understood as an expansion of productive capacity, which requires investment in physical capital, infrastructure, and human capital. In order for investment to take place, resources must first be freed from current consumption, which makes saving a necessary precondition for investment.

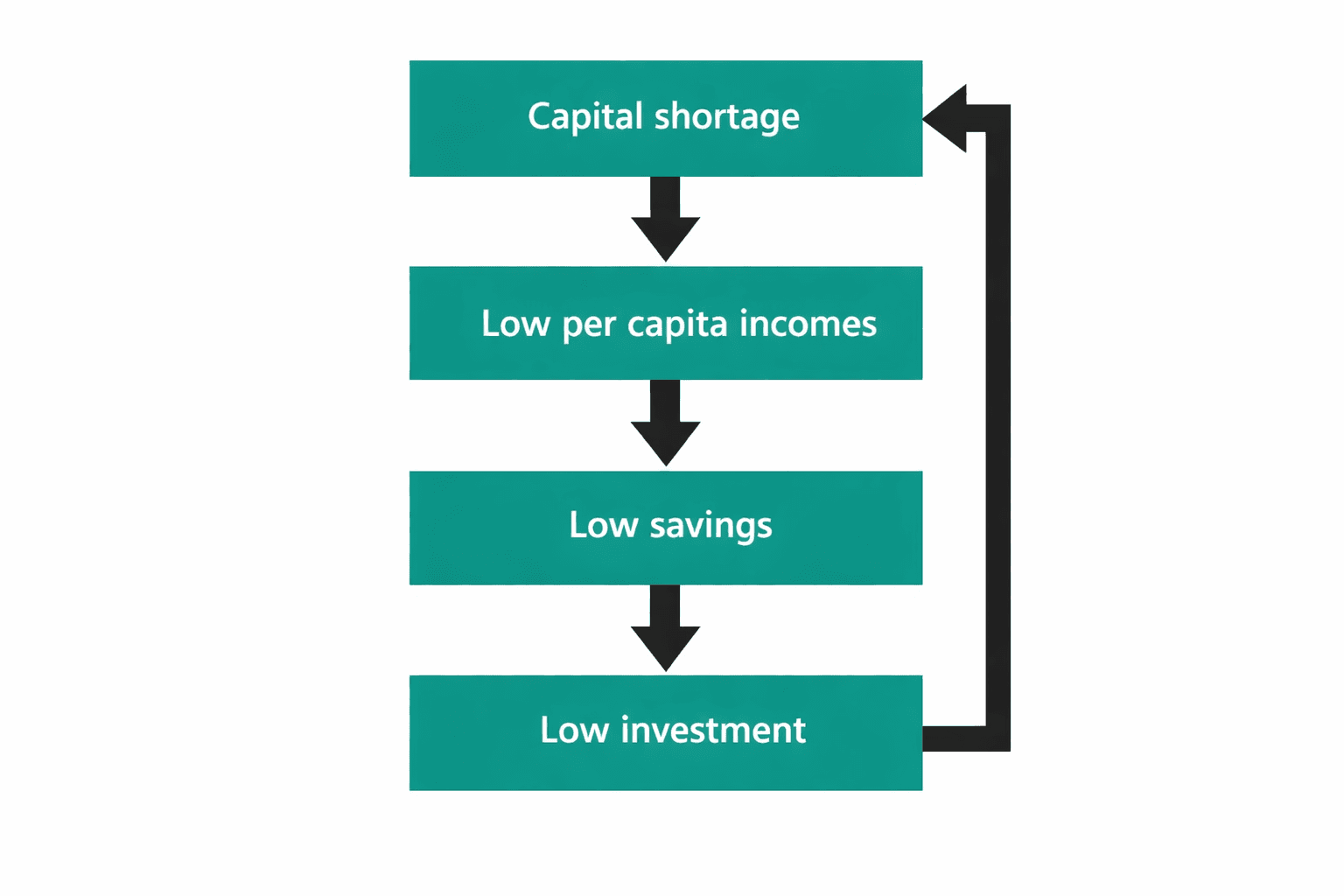

Many developing countries face a shortage of capital, reflected in low levels of capital per worker and low productivity. Low productivity contributes to low incomes, which in turn restricts the capacity of households to save. When saving is low, the funds available for investment are limited, resulting in low levels of capital accumulation. This reinforces low productivity and low incomes, creating a self-reinforcing cycle. This situation is often described as a low-level equilibrium trap, in which the economy remains stuck at a low level of income and output because saving and investment are insufficient to generate sustained growth.

The financial sector plays a critical role in determining whether this cycle can be broken. Even when some saving exists, it must be effectively mobilized and transformed into investment. Where financial institutions are underdeveloped, savings may be held in unproductive forms or may fail to reach firms with profitable investment opportunities. As a result, the sacrifice of current consumption does not translate into future gains in output and income, weakening incentives to save further.

In addition to the quantity of saving, the efficiency with which savings are allocated matters for growth. Investment that raises productive capacity requires access to appropriate physical capital, technology, and skilled labor. Where firms lack access to finance, even high-return investment projects may not be undertaken. This highlights the importance of a financial system that can identify productive opportunities and channel funds accordingly.

The Harrod–Domar model

The importance of saving and investment in the growth process is emphasized by the Harrod-Domar model of economic growth. This model was developed to explain how economies can achieve steady growth over time and to identify the conditions under which growth is stable or unstable.

At its core, the model links economic growth directly to the rate of saving and the productivity of capital.

The model suggests that an economy can remain in equilibrium only if it grows at a rate determined by the saving rate and the capital-output ratio. If actual growth deviates from this required rate, the economy may become unstable. This finding underscores the importance of maintaining sufficient levels of saving and investment to sustain growth.

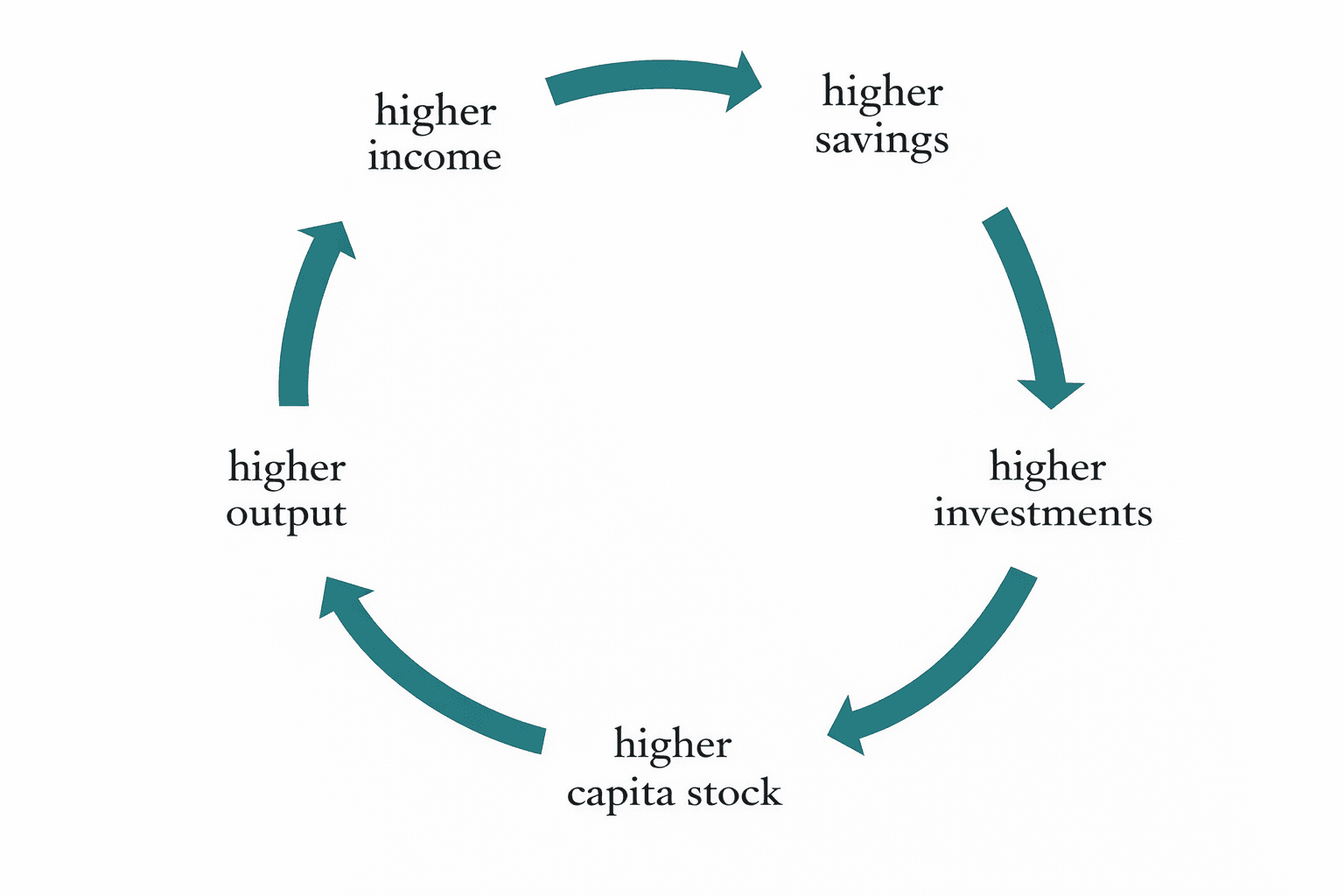

In the context of developing economies, the Harrod–Domar model highlights the central role of capital accumulation. Investment increases the stock of capital, which raises productive capacity and output. Higher output leads to higher incomes, which can then support higher saving. In this way, growth can become self-sustaining once the initial constraints on saving and investment are overcome.

However, the model also illustrates why growth can be difficult to initiate. If saving is too low or if capital is used inefficiently, investment will be insufficient to generate the growth needed to raise incomes significantly. This reinforces the importance of a well-functioning financial sector that can mobilize savings and ensure that investment is productive.

External resources and development

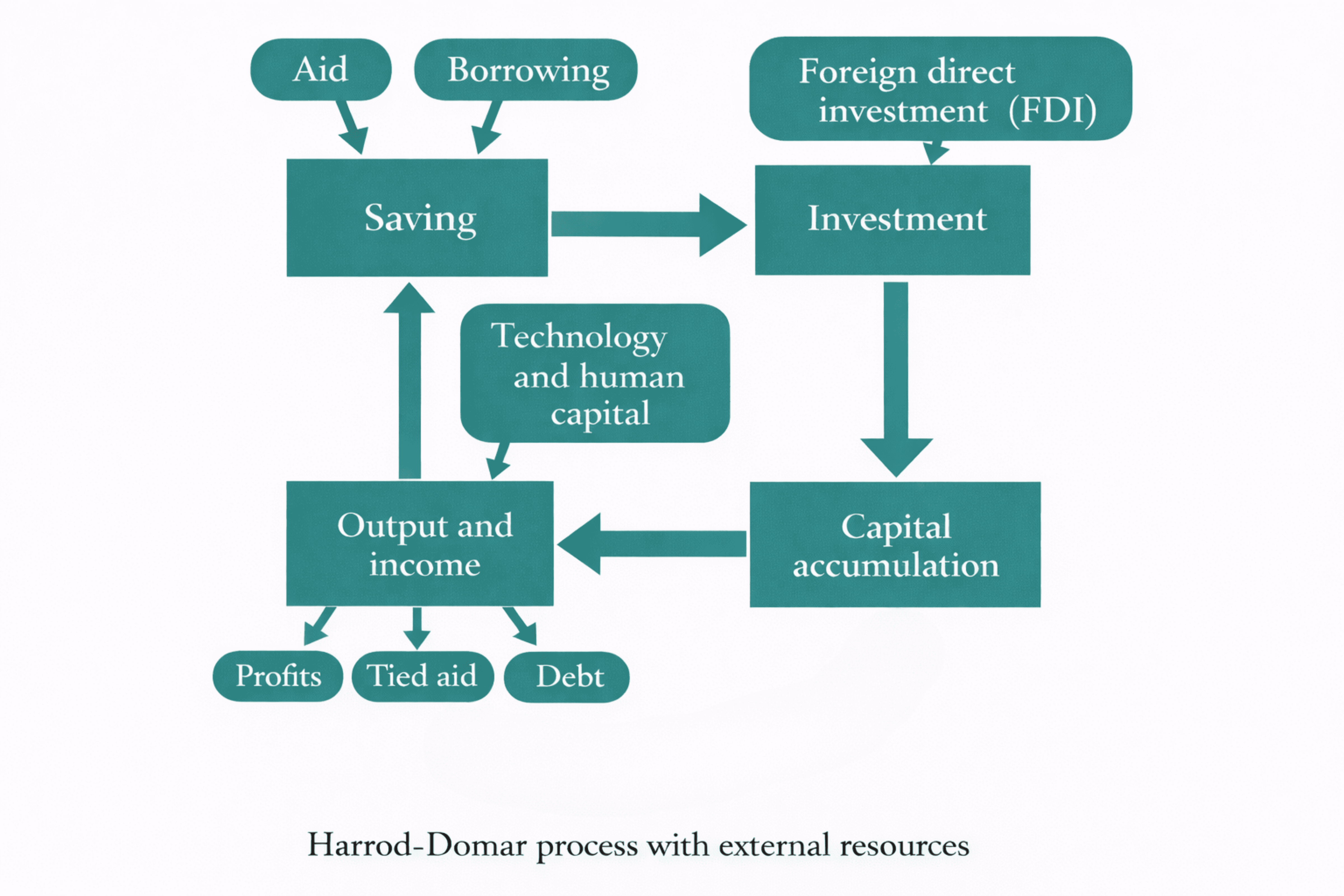

For many developing countries, domestic saving alone may be insufficient to finance the level of investment required for rapid growth. In such cases, external sources of finance can supplement domestic resources. These external resources may take the form of foreign direct investment, international borrowing, or overseas assistance.

Foreign direct investment can provide not only financial capital but also access to technology, managerial expertise, and international markets. This can enhance productivity and accelerate growth, provided that profits are reinvested domestically rather than repatriated entirely. International borrowing can also finance investment, but it creates future obligations in the form of debt servicing, which may become burdensome if growth does not materialize as expected.

Reliance on external finance introduces additional risks. Some forms of external funding may not be used efficiently, and large inflows of funds can create dependency or distort incentives. Moreover, debt accumulation can become unsustainable, particularly if borrowed funds are not invested productively. These risks highlight the importance of sound financial management and effective institutions.

Microfinance and access to credit

In many developing economies, access to finance is particularly limited for small-scale projects, especially in rural areas. Formal financial institutions may be unwilling or unable to lend to small borrowers due to high transaction costs, lack of collateral, and difficulties in assessing creditworthiness. As a result, individuals and small enterprises may rely on informal lenders who charge very high interest rates.

Microfinance schemes have emerged as one response to this problem. These schemes provide small loans to individuals who would otherwise lack access to credit, often without requiring traditional collateral. By targeting small-scale income-generating activities, microfinance aims to support entrepreneurship, raise incomes, and reduce poverty.

One influential example is the Grameen Bank, which pioneered group-lending arrangements in which borrowers are jointly responsible for repayment. This structure reduces default risk by creating social incentives to repay loans and lowers monitoring costs for lenders. Microfinance initiatives have achieved high repayment rates and have expanded access to credit for many individuals, particularly women.

Despite these successes, microfinance is not a complete solution to the challenges of development finance. Some schemes rely on subsidies to remain viable, and the impact of microfinance on long-term growth and poverty reduction varies across contexts. Nevertheless, microfinance illustrates how innovative financial arrangements can address market failures and expand access to finance.

Evaluation of the financial sector in development

An effective financial sector is a necessary condition for economic growth and human development, but it is not sufficient on its own. Financial institutions must be complemented by investments in physical infrastructure, education, and healthcare in order to raise productivity and living standards. Where financial markets function well, resources can be directed toward their most productive uses, supporting growth and development.

In many emerging economies, progress has been made in strengthening financial systems and expanding access to finance. However, significant challenges remain, particularly in regions where formal financial institutions are weak or absent. Addressing these challenges requires institutional development, regulatory capacity, and policies that promote financial inclusion.

Overall, the financial sector plays a central role in mobilizing savings, facilitating investment, and supporting economic growth. Its effectiveness has important implications for development outcomes, making it a critical focus of economic policy in both developing and advanced economies.

Next Article