Private Credit poses a major risk to investors, but the current controls may also be the last thing that stops it from becoming another 2008-style crisis

The current conditions of the US private credit market may sound alarms for some, as it is a highly illiquid market for private lending that operates completely outside traditional banking structures. $13 trillion of capital. Recent fears of defaults at some of the largest funds. Cappings of redemptions. Informality and flexibility in negotiations of loan terms and conditions. “Opaque” exposure to these loans from banks, according to Bank of America’s Head of Global Research, Barnaby Martin. Recent requests from the SEC to learn more about the poorly understood scale and operations of this fixed-income asset class.

This might sound like the recipe for a credit disaster akin to that of 2008, but the features above are actually the exact reasons why private credit, unlike mortgage-backed securities (MBSs) and collateralized loan obligations(CLOs), does not pose a systemic risk to the financial sector. Systemic risk differs from idiosyncratic risk in that it represents the risk of cascading failures across the financial sector caused by (sometimes hidden) interlinkages and interdependence, such as the cascading failures of MBSs in the 2008 financial crisis.

After the Great Financial Crisis of 2008, banks moved away from private lending due to regulatory and balance sheet concerns. This left a void to be filled by Private Credit, which increasingly lent to business development companies (BDCs) with more flexible terms and faster financing than traditional banks, often at a higher premium. This grew into what is often termed the Golden Age of private credit, in which investors could expect returns above market rates on senior secured debt.

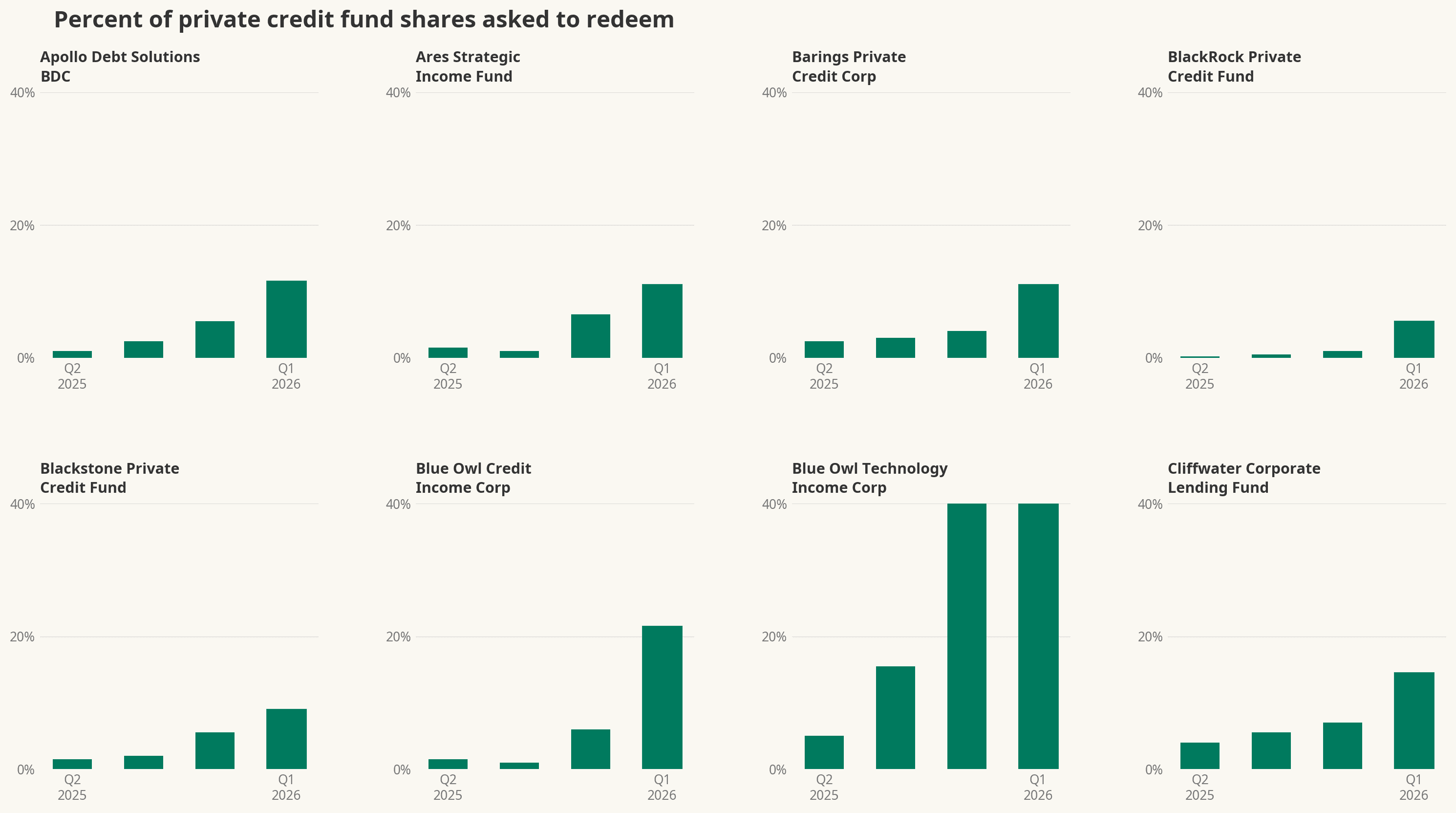

However, recently, alarm bells have started to sound, mostly due to fears of overinvestment of private credit funds in the wake of an AI-Powered “SaaSpocalypse”. For example, one of the premier private credit funds, BlackRock Private Credit(BCRED), lends 26% of its portfolio to software companies. Withdrawal requests have been high from BCRED (~8%), but higher (22%) from Blue Owl Capital, which has 70% of its capital lent to software. Blue Owl Capital’s private credit fund has become the poster child for the rapid run-up in private credit funds heavily invested in software.

However, despite steep withdrawal requests, most firms are structurally illiquid, hard-capping redemption requests at 5% quarterly at most firms. Some firms, like Blue Owl Capital, have exceeded the cap to appease investors, but many firms like BCRED have remained firm with BlackRock CEO Larry Fink stating, “It's not like it's on Page 92 of a prospectus. It's on Page 1,” regarding the 5% redemption request cap.

While it might seem scary to have funds locked up in a failing investment, these redemption request caps are exactly what’s preventing institutional investors, banks, and life insurance funds invested in private credit from taking the heaviest losses. If redemption requests were not capped, the fund's value could essentially be reduced to zero as more and more investors cash out, forcing it to sell off its current positions and no longer producing the returns promised to investors. This is also a strong differentiating factor from 2008, where huge, systemic runs on MBSs and CLOs left institutional and retail investors and pension funds crippled.

Additionally, Private Credit usually positions itself as the most senior debt and has strong covenants that require businesses that fail to meet benchmarks to take certain actions. This means that both equity would have to dry up and businesses would have to fail so quickly as to disallow correction by the BDC. This is a much stronger position than subprime lending, which provided predatory loans to unreliable individuals in the run-up to 2008.

Finally, the Private Credit market is much less intertwined with the greater financial system than MBSs were in 2008. Sure, some banks do have investments in Private Credit, but these investments rarely exceed 5% of the bank's holdings, and they’re protected from runs for the reasons mentioned above. Additionally, Private Credit is only (currently) available to very affluent or institutional investors, keeping losses contained and away from the general public.

These safeguards protect investors and prevent greater crises, except in one distinct possible future scenario in which private credit investments become accessible to retail investors, and funds become more liquid, driven by increasing demand. This isn’t the reality now, but under the Trump Administration, the SEC is currently advancing policies to bring private investments (like Private Credit) into public availability. If this were to occur, and funds were exposed via highly liquid instruments to public investors, a true private credit run could be triggered, and funding for lower and middle-market businesses across the country could dry up, or losses would be shifted directly onto Main Street.

Ideally, this isn’t the case, as the last few months serve as a warning about the dangers of investing in private credit and the importance of illiquidity for long-term investments. In the meantime, while the current private credit market may cause some damage to institutional and affluent investors, their returns are protected by its structural elements, which also keep the greater economy insulated from negative systemic effects.