AI driven layoffs and immigration crackdowns are hitting the labor market at once. As white- and blue-collar jobs disappear, weakening consumer confidence threatens the spending that underpins the American economy.

Amazon, Block, Accenture, Atlassian. Each week brings a new headline: another major company laying off a large portion of its white-collar workforce and citing AI integration as the reason. At the same time, the construction sites and hospital wards that have until now propped up US job growth are threatened by the deportation of the immigrant workforce that staffs them. These are two structural shocks hitting the US labor market simultaneously, and together they pose a serious short-term threat to consumer spending, which drives the American economy.

Even before these twin shocks took hold, Fed Chair Jerome Powell observed at the August 2025 Jackson Hole Symposium that the labor market was exhibiting unusual fragility: payroll growth had stalled and job gains were narrowing sharply. Monthly payroll growth had slowed to an average of just 35,000 jobs (down from 168,000 per month in 2024) and the unemployment rate for recent college graduates had climbed to 4.8%, above the national average for the first time in decades. With 92,000 jobs lost this February and growth already concentrated in just a few sectors, the labor market was poorly positioned to absorb the disruptions now arriving from two directions at once.

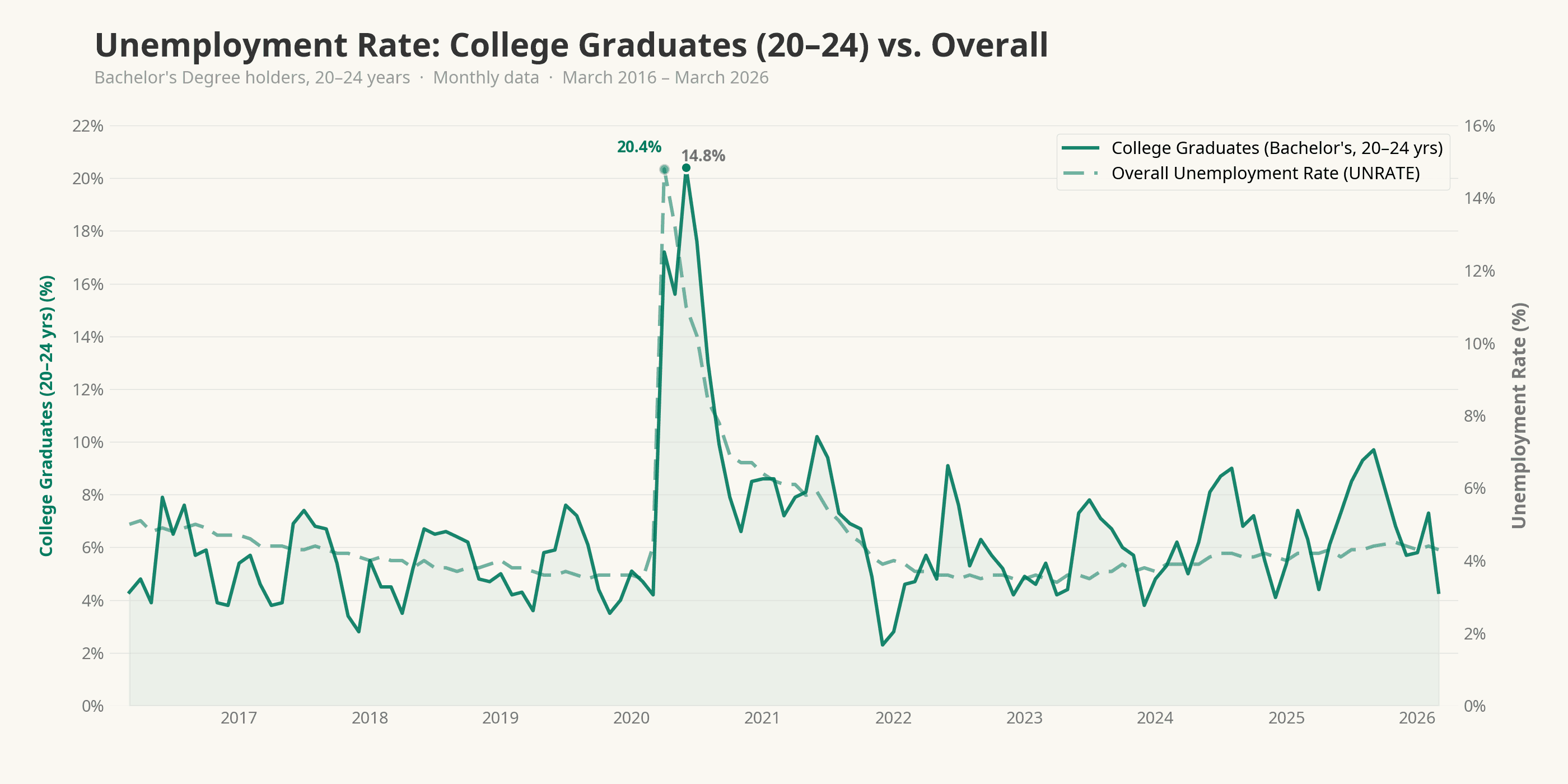

The graph above shows a worsening labor market for recent college graduates. Historically, college graduates have had a similar unemployment rate to the general population. In the past 3 years, recent college graduates have consistently had higher unemployment than the general population, with unemployment rates rising to 9.7% in September and currently at 7.8%.

This demonstrates labor market tightness by showing the narrowing (and now closed) gap between the unemployment rate and total nonfarm job openings. A rising unemployment rate over the past three years and a decreasing number of positions spell bad news for the labor market.

The first shock is AI-driven displacement. In the long term, AI may drive economic growth, increase productivity, and lead to better overall outcomes. However, recent disruptions have been short-term and fast-paced: Claude Code has effectively reduced the need for entry-level programmers, and modeling plugins could significantly reduce demand for financial analysts. According to Challenger, Gray & Christmas, AI was cited as a factor in approximately 55,000 US layoffs in 2025 alone — more than 12 times the figure from just two years prior, the sharpest single-year acceleration on record. This is white-collar displacement happening at unprecedented rates.

The second shock is playing out across sectors AI hasn’t touched: healthcare, hospitality, and construction. The industries that, until recently, propped up overall job growth and employ the highest proportions of immigrant workers. Construction draws roughly 30% of its workforce from foreign-born workers; immigrants account for approximately 15.6% of nurses and 27.7% of health aides nationwide. Recent sweeping deportations and immigration enforcement, triggering an 80% decrease in net immigration, have left these sectors acutely exposed. While conventional logic suggests deportations should open job positions for American citizens, the opposite may actually be true: employers are shutting down operations entirely due to labor shortfalls, a dynamic that may help explain the February job losses in these sectors.

Together, these two shocks converge on the same pressure point: consumer spending. In the United States, aggregate demand is driven by one thing, and firms appear to be discounting this reality as they slash jobs to shore up margins. Workers are consumers, and structurally displaced workers are pessimistic consumers without the means to contribute to the greater macroeconomy. Moreover, even workers who retain their positions become cautious spenders when they perceive broader labor market instability. Consumer spending accounts for roughly 70% of US GDP, which means a structurally weakened labor market translates intrinsically into a weaker economy.

The data is already reflecting this. The Conference Board’s Consumer Confidence Index fell to 84.5 in January 2026, a 12-year low, while the University of Michigan Consumer Sentiment Index stood at 57.3 in February 2026, approximately 20% below its January 2025 level. The disconnect between headline GDP growth and collapsing consumer sentiment points directly to a labor market that is structurally weakening from both ends: white-collar jobs lost to AI, blue-collar jobs lost to deportation-driven labor shortfalls. These numbers could be backward-looking, but they could also signal potential reduced spending to come.

This is ultimately a governance problem. Two structural shocks are eroding the labor market simultaneously, and neither is being managed with the seriousness the stakes demand. AI displacement and immigration enforcement are being driven by firm-level profit motives and executive policy priorities, respectively, with little regard for their combined effect on the consumer demand that underpins the entire US economy. Even if AI proves beneficial in the long run, combined with unrestrained immigration enforcement, the short-term damage to workers and the spending power they represent could be severe and lasting.